Capital gains on double-tier partnerships in trade tax

The taxation of double-tier partnership structures is extremely complex when selling co-partner shares, especially if shares in the superior partnership are sold but hidden reserves exist in the subordinate partnership. This is because the seller realizes a capital gain from his co-ownership, which consists of the superior and subordinate partnerships, each with its own business assets. Against this background, the German Federal Fiscal Court had to clarify, among other things, in its ruling of May 8, 2025, case no IV R 40/22, whether such a capital gain must be allocated to the business income of the superior and subordinate partnerships.

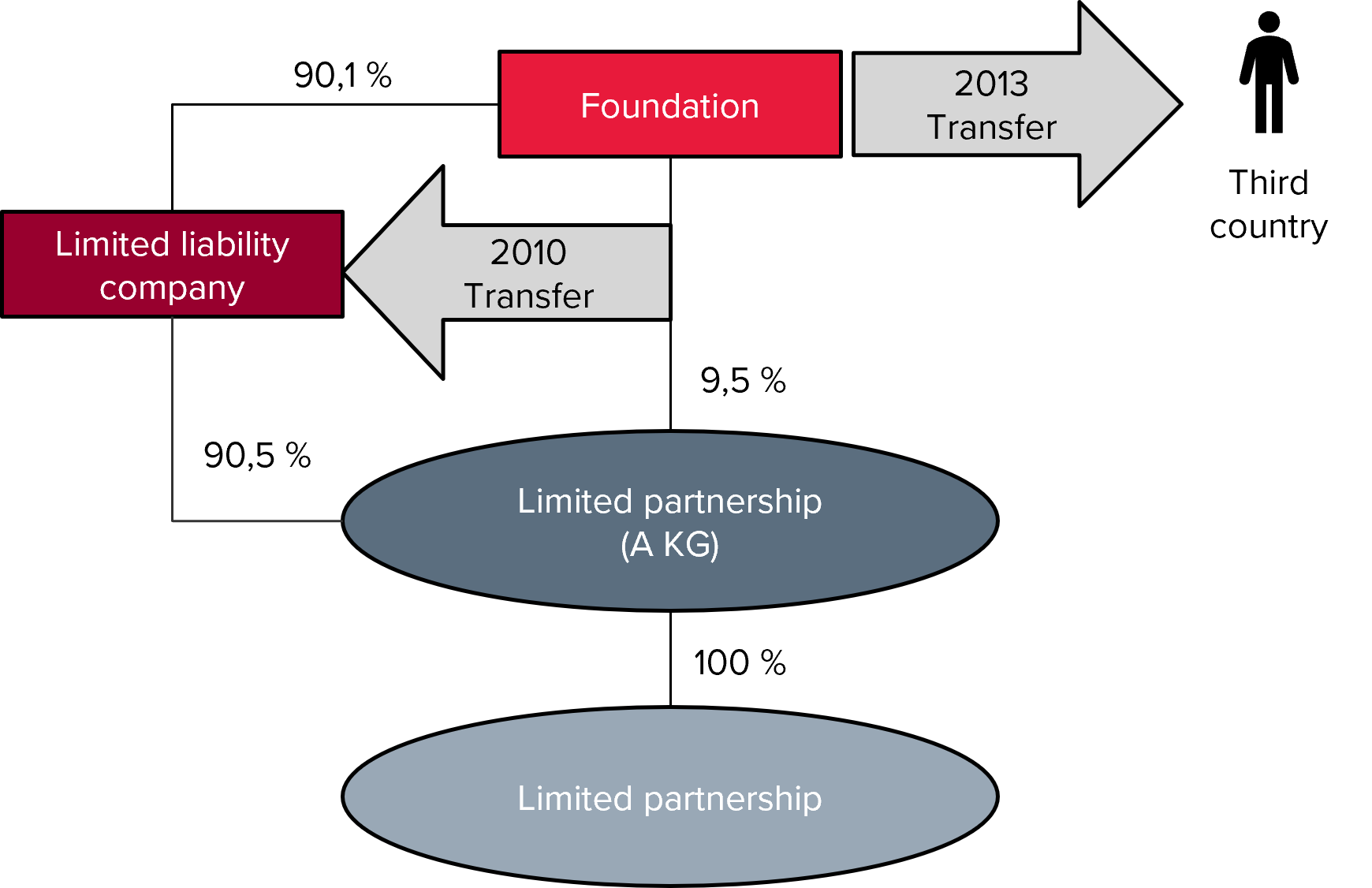

In the case in dispute, a limited partnership (A KG) held interests in various other limited partnerships, most of which operated hospitals and clinics. The limited partners of A KG were a limited liability company with a 90.5 % stake and a foundation with a 9.5 % stake. The foundation also held a 90.1 % stake in the limited liability company. In 2010, the foundation transferred its stake in A KG at book value to the limited liability company in exchange for new shares (Section 20 (2) sentence 2 of the German Transformation Tax Act (UmwStG)). In 2013, the foundation’s assets, including the stake in the limited liability company, were transferred to a natural person living in a third country.