Aktuelles

Datum:

Between 2025 and 2027, the European Central Bank (ECB) is sharpening its supervisory lens on geopolitical risks, introducing new measures to assess banks’ resilience to external shocks. This includes evaluating transmission channels across financial markets, real economic activity, and policy dimensions. A notable rise in on-site supervisory activity - now accounting for 55% of all ECB action - demonstrates intensified scrutiny, especially in areas like credit risk governance, expected credit loss (ECL) modelling, liquidity stress testing, and internal control functions.

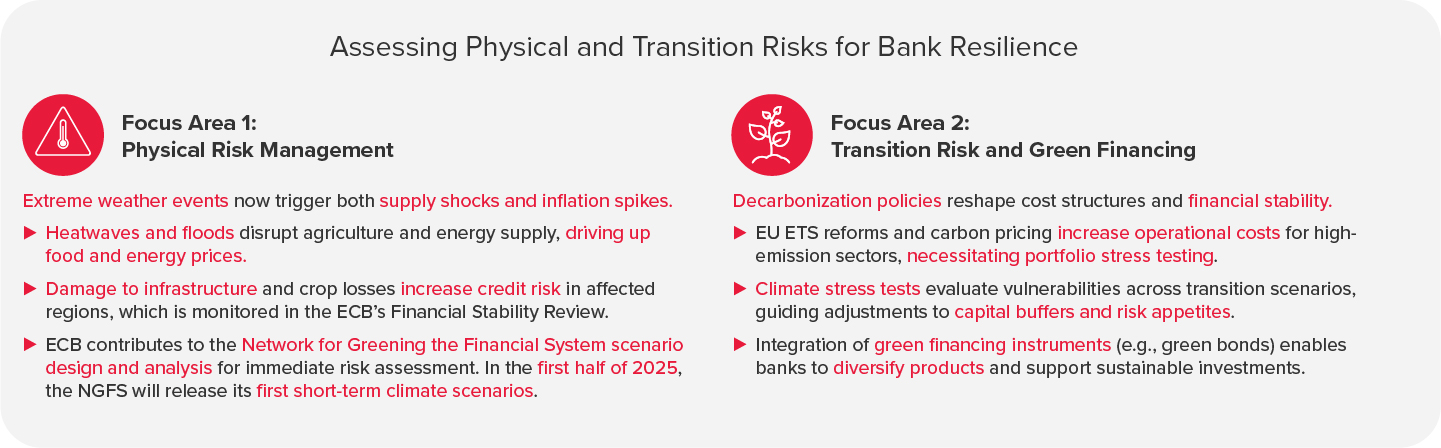

Key findings from recent inspections expose serious deficiencies, including flaws in risk quantification, inadequate data quality, weak cyber risk defenses, and inconsistent integration of climate risks into core strategies. Supervisory expectations are rising - banks must enhance their governance, improve risk models, and embed ESG criteria more comprehensively.

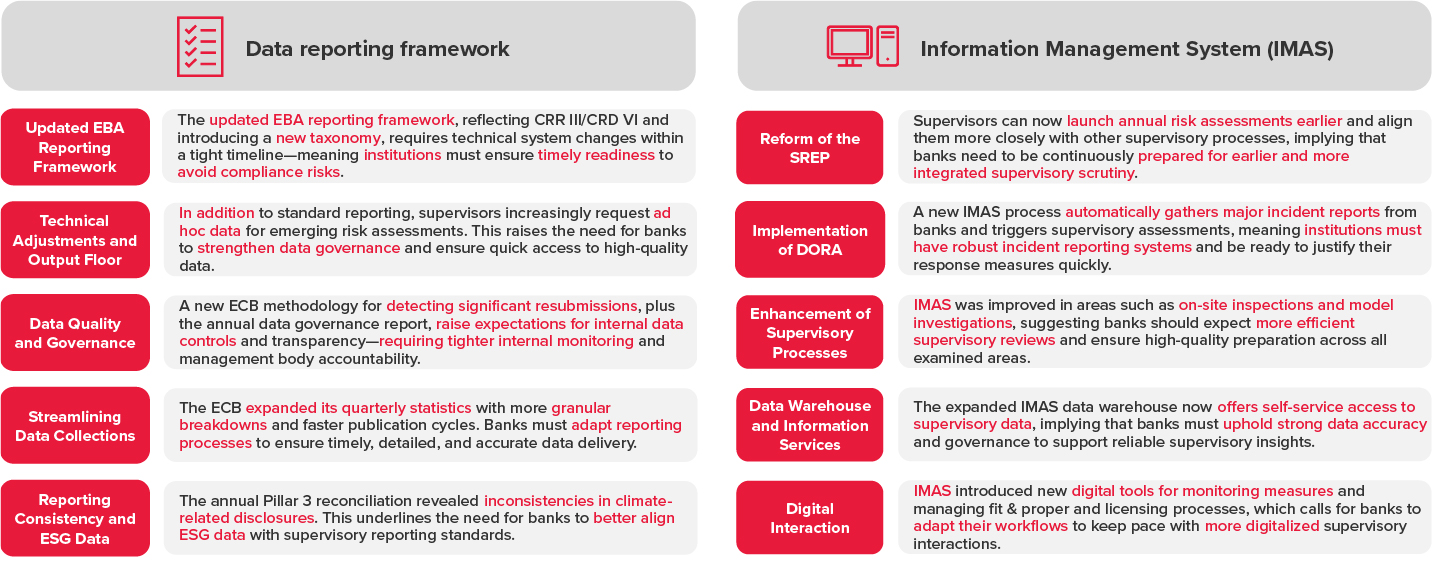

Simultaneously, the ECB is overhauling its data interaction systems. Enhanced IMAS capabilities and data warehouses now demand faster, more accurate reporting, particularly as ad hoc supervisory data requests increase. The implementation of the Digital Operational Resilience Act (DORA) and new ESG disclosure requirements only add to this pressure.

On the monetary policy front, despite inflation moderating to 2.4%, the ECB maintains a restrictive approach, with the discontinuation of liquidity-support programs like TLTRO and asset reinvestments impacting funding strategies. Additionally, the ECB advances its digital euro project—framed to ensure monetary sovereignty, payment system resilience, and privacy.

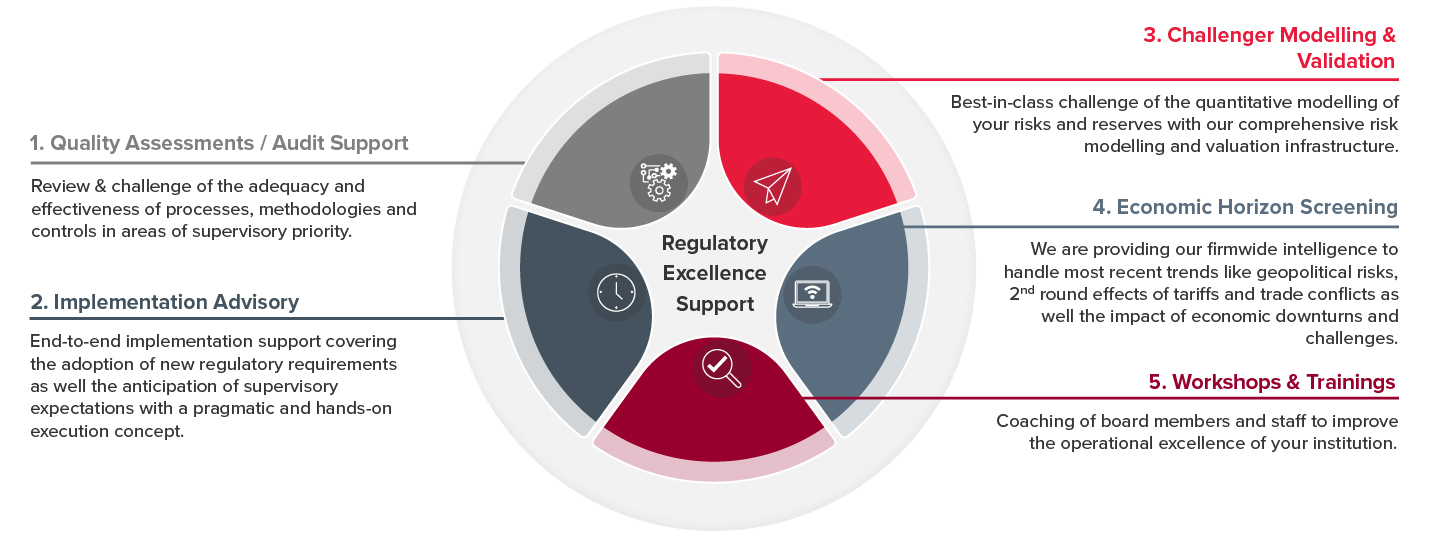

In this evolving landscape, BDO offers strategic advisory support, ranging from ECB onboarding readiness and model validation to geopolitical risk screening and ESG integration. Their pragmatic, hands-on approach positions them as a trusted partner for navigating regulatory complexity with confidenc

Launch of new supervisory initiatives in the area of geopolitical risks

The ECB plans to further heighten its scrutiny regarding banks‘ resilience to geopolitical shocks and will address this in the 2025-2027 cycle with the following supervisory initiatives:

Transmission channels of geopolitical shocks to banks:

Geopolitical shocks can affect the banking sector through a range of interconnected transmission channels that span both macro-financial impacts and institution-specific vulnerabilities. On a macro level, such shocks can lead to widespread asset repricing, including commodities, equities, and sovereign bonds, often triggering a flight to safety and reversal of capital flows. This is frequently accompanied by wider sovereign spreads and disruptions to cross-border payment systems. Moreover, there are downside risks to global growth and trade, increased inflationary pressures, exchange rate volatility, and concerns over public debt sustainability. Physical and operational threats, such as damage to infrastructure, military conflict, cyberattacks, and disinformation, further compound these risks, particularly in regions with institutional fragility or socioeconomic instability.

These broad macro shocks translate into bank-specific vulnerabilities across several risk categories:

This comprehensive framework illustrates how geopolitical turbulence propagates through financial systems, prompting the ECB to prioritize banks’ resilience to geopolitical shocks in its supervisory agenda for 2025–2027. The supervisory approach includes forward-looking assessments and targeted measures across these risk domains.

Between 2023 and 2024, the ECB maintained a high volume of supervisory measures, with a total of 5,465 measures recorded. Of these, a significant 44.9% (2,453 measures) were linked to on-site inspections and internal model investigations. This reflects a notable increase in on-site supervision in 2024, while off-site activities experienced a slight decline relative to other categories. In particular, on-site inspections and internal model investigations—most of which are conducted in person—emerged as the dominant supervisory tools, together accounting for 55% of all measures in 2024. This shift underlines the ECB’s intention to deepen its scrutiny through direct engagement with supervised institutions.

The other supervisory activities included follow-ups on previous measures (27.8%), ongoing supervision (23%), and other actions such as thematic reviews and enforcement (4.3%). The elevated proportion of follow-up measures demonstrates the ECB’s continued focus on ensuring that previous findings are adequately remediated. Overall, these trends indicate a more hands-on, risk-focused supervisory stance, with an emphasis on resolving persistent weaknesses through active engagement.

Number of measures recorded (2017-2024):

Between 2017 and 2024, the total number of supervisory measures imposed by the ECB remained consistently high, averaging around 7,500 measures annually. These figures reflect the ECB’s steady and proactive supervisory stance over the years. Importantly, about half of the measures issued were classified as severe, underscoring the ECB’s commitment to addressing material weaknesses in supervised institutions.

In 2024, the ECB recorded an average of 66 measures per bank, a significant increase from 52 measures per bank in 2022. This rise indicates a more intensive and tailored supervisory engagement, likely reflecting the ECB’s heightened focus on resilience amid increasing macro-financial and geopolitical risks. The figure shows that this intensification followed a dip in 2021, with supervisory activity rebounding sharply in 2022 and remaining at a higher level since then. The upward trend also suggests that banks are subject to more granular and frequent assessments, particularly in areas like internal governance, risk management, and operational resilience.

Overall, these trends reveal not only a consistent level of supervisory intervention but also a rising emphasis on supervisory intensity and enforcement across the euro area banking sector.

As of 2024, the number of less significant institutions (LSIs) in the euro area continued its gradual decline, reaching a total of 1,912 entities. This reduction is primarily attributed to structural changes driven by mergers, reflecting ongoing consolidation in the sector. Despite this shrinking population, the business models of LSIs remain highly heterogeneous, with institutions differing considerably in terms of size, regional footprint, and focus areas.

The classification by business model reveals that retail and consumer credit lenders continue to dominate the LSI landscape, accounting for approximately 60% of all LSIs. This category includes institutions focused on personal loans, mortgages, and other consumer-facing credit products. Nevertheless, other business models such as diversified lenders, corporate/wholesale lenders, custodian and asset managers, and development/promotional lenders are also represented to varying degrees, often depending on national banking structures.

There is a clear regional concentration of LSI activity, with certain Member States hosting large numbers of institutions. Germany stands out as the country with the highest concentration of LSIs, significantly surpassing others in terms of both absolute number and institutional diversity. Countries like Austria, Italy, and France also have sizeable LSI sectors, though with different business model compositions.

The observed distribution illustrates the persistent fragmentation of the LSI landscape across the euro area, underscoring the need for continued monitoring and harmonization efforts by national competent authorities and the ECB.

Germany has by far the largest share of less significant institutions (LSIs) in the euro area, accounting for 42% of the total. Austria and Luxembourg also host large LSI populations, each representing more than 1% of all LSIs and a market share above 25%. In contrast, many countries, including France, Belgium, and Greece, have both a small number and a low market share of LSIs. Several national supervisory authorities apply pooled or multi-pooled structures for ICT risk supervision, while others rely on non-pooled frameworks. In some jurisdictions, LSIs use concentrated IT systems, and several countries have transposed EBA ICT risk guidelines into national law. This highlights the diverse supervisory environments and technological setups across the euro area.

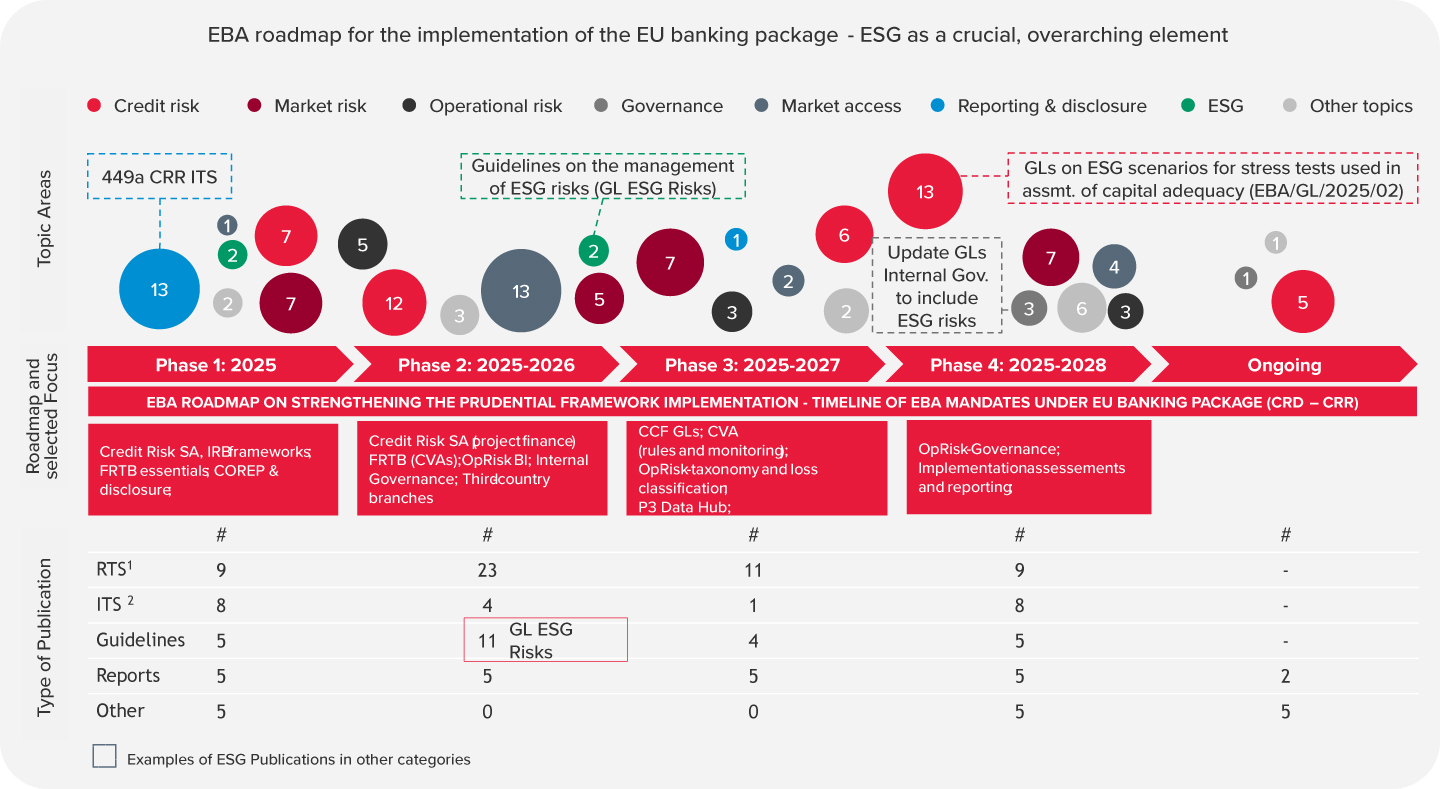

Within supervisory efforts for a lean, efficient, and standardized as well as unified reporting regime in Europe, various initiatives require attention:

(Core)Inflation continues to evolve towards the inflation target of ~ 2%, albeit uncertainty remains high.

Inflation Developments and Their Monetary Policy Context

Physical as well as transitional C&E-risks are to be integrated into the overarching strategic objectives of the ECB and are an established focus topic within the banking supervision in Europe.

The ECB strives towards a digital euro while keeping the commitment to cash:

The Euro is internationally well established, albeit diversification trends and non-traditional currencies gain ground. A resilient financial market infrastructure as well as accountability and transparency as a trustworthy institution remain areas of high attention.

Strengthening the Euro’s International Role

Ensuring Cyber Resilience in the Financial System

Accountability and Institutional Transparency

As a trusted advisor, well established sparring partner, and experienced service provider, BDO has the answers and solutions for your future excellence. Selected services are.

Sources / References used within this article: